IREN, 비트코인 채굴에서 MS 13조 계약사로 — $50 돌파 운명의 일주일 IREN, 비트코인 채굴에서 MS 13조 계약사로 — $50 돌파 운명의 일주일 필자가 키움증권 상위 랭킹에서 우연히 발견한 종목, IREN(아이리스 에너지) 입니다. "왜 이 종목이 갑자기 위에 떠 있지?" 궁금해서 차트를 열었더니, 긴 하락 채널 상단에 정확히 맞닿아 있는 자리 였어요. 이번 주 안에 거래량 동반 돌파가 나오면 단숨에 $59~$62까지 슈팅, 실패하면 채널 안으로 회귀해 $45 일목 구름까지 밀릴 수 있는 구간. 그런데 차트 너머로 더 흥미로운 게 보입니다 — 마이크로소프트와 약 13조 6천억원($9.7B) AI 인프라 계약 을 체결한 회사라는 사실이에요. 📌 키움증권 상위 랭킹에서 발견 — "왜 이 종목이?" 안녕하세요, 30대 진도리에 취미생활 의 미니도리몽입니다. 📋 필자 발견 경로 + 현재 포지션 · "자리 괜찮은 종목 좀 골라보자"하고 키움증권 상위 랭킹 살피던 중 IREN 발견 · 차트 열어보니 $50 부근, 하락 채널 상단 에 정확히 도달 · 현재 미보유 , 차트 돌파 여부 확인 후 본주 분할매수 검토 중 국내 투자자분들도 비슷한 경험 있으실 거예요. 증권앱 상위 랭킹에 갑자기 올라온 종목, 무심코 넘기기보단 한번 들여다봅시다. 상위 랭킹에 뜨는 데는 보통 거래량·등락률·유입자금 같은 시그널 이 있거든요. 이번 글의 흐름은 다음과 같습니다. ① 빅테크 AI 투자비 812조원의 진짜 종착지 — 왜 NVDA가 아니라 IREN 같은 데이터센터 운영사인가 ② 마이크로소프트 약 13조원 계약 — 변신의 결정적 증거 ③...

공유 링크 만들기

Facebook

X

Pinterest

이메일

기타 앱

Apple 2025 Stock Analysis: Risk Reassessment, AI Competition, and ETF Impact

공유 링크 만들기

Facebook

X

Pinterest

이메일

기타 앱

📌 Key Takeaways (3 Lines)

Apple (AAPL) has declined about 24% YTD in 2025 and is now regarded as a risk asset among tech stocks.

The stock is exposed to political, tech, and legal risks such as Trump’s tariff rhetoric, AI competitiveness concerns, and DOJ investigations.

Institutions have started to reduce or rebalance their positions; investors with heavy ETF exposure to Apple should be extra cautious.

📌 AI Content Notice

This post was created using ChatGPT summarization, combined with the author's interpretation and editorial input.

All included charts and scores are subjective analyses based on publicly available data. These are not investment recommendations and should be used for informational purposes only.

📌 2025 Investment Analysis: Apple (AAPL) – From Tech Icon to Risk Asset?

🧠 Author’s Thoughts

Personally, I believe the smartphone and tablet markets have peaked. Most recent launches are high-end and expensive enough to rival premium laptops or appliances. Performance improvements have slowed dramatically, and most users do not require that much power in daily use.

Therefore, future smartphone growth must be driven by AI integration. But will leading AI firms like OpenAI or Google need to collaborate with Apple or Samsung? It’s increasingly possible that AI-centric companies will design and control their own hardware, ecosystems, and infrastructure. Recent moves by Jony Ive and OpenAI support this view.

That’s why I believe even Apple’s premium and tech leadership status may need a fundamental reassessment. This post is my attempt to reevaluate Apple’s position in my long-term holdings list.

📋 Company Overview & Fundamentals

Company: Apple Inc.

Ticker: AAPL (NASDAQ)

Sector: Technology / Consumer Electronics

Market Cap: Approx. $3 trillion (2025)

Main Products: iPhone, iPad, Mac, Apple Watch, AirPods, Apple Services (App Store, iCloud, Apple TV+ etc.)

Apple is one of the world’s most recognized tech companies, generating revenue from premium consumer electronics and an expanding services ecosystem. iPhone still contributes over half of total revenue, while software and service sales continue to grow. Recently, boosting AI competitiveness and forming strategic partnerships have become urgent tasks.

As of 2025, Apple is widely considered to have entered a “valuation recalibration” phase. Its PER stands at 27.4x, a middle ground compared to Microsoft and Alphabet, showing Apple still commands a market premium.

Apple’s weight in ETFs is significant: QQQ (12.3%), VOO (6.9%), SPY (7%), XLK (22%), etc. Such heavy inclusion means short-term declines can trigger technical selling pressure, so ETF-heavy investors should remain vigilant.

📉 Market Reaction Summary

Year-to-date stock decline: approx. -24.1%

Increased market sensitivity to key issues:

Trump’s tariff remarks: -3% drop

OpenAI rivalry headlines: additional -2% drop

DOJ antitrust risk: sustained weakness

📈 Analyst Ratings & Target Prices

Firm

Target Price

Upside Potential

Comment

Morgan Stanley

$220

+12.7%

Optimism about H2 AI chip launch

JP Morgan

$210

+7.6%

Slower revenue growth expected

Bank of America

$200

+2.4%

App Store monetization pressure

Citi Group

$195

±0%

Neutral valuation

📊 Stock Charts (TradingView Reference)

1-Day: $195.27 (as of May 23)

1-Month: -12.6%

1-Year: -24.1%

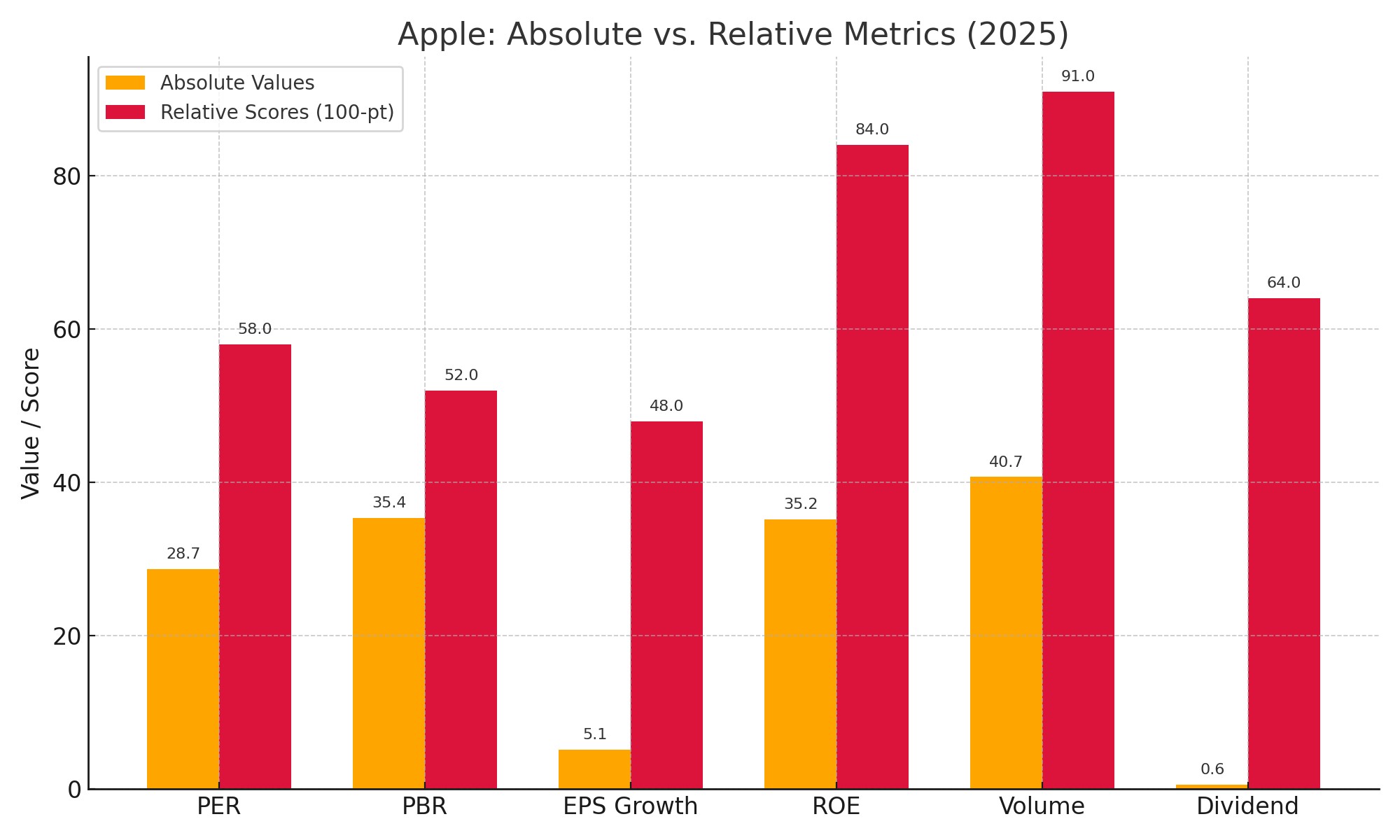

📊 Key Financial Metrics (2025)

Metric

Score (out of 100)

Description

PER

58

Correction phase, lower growth reflected

ROE

84

Excellent capital efficiency

FCF Margin

77

Strong cash flow

Dividend Yield

64

Slightly up, still relatively low

Debt Ratio

70

Stable financial structure

Volume Change

91

Increasing sell-off, stop-loss signals

📈 Radar Chart Score: 74.0 / 100

A visualized investment score based on six major financial metrics

* This chart includes PER, PBR, ROE, EPS growth, dividend yield, and volume change, normalized out of 100, sourced from Investing.com and Yahoo Finance.

Visual comparison between raw metrics and standardized scores (100-point scale)

🔍 Peer Comparison: Apple vs Microsoft vs Alphabet vs Amazon

Metric

Apple

Microsoft

Alphabet

Amazon

PER

27.4x

32.1x

23.7x

61.2x

ROE

155%

42%

30%

21%

FCF Margin

25%

34%

22%

10%

Market Cap

$3.01T

$3.14T

$1.9T

$1.8T

* As of May 2025, source: Investing.com & Yahoo Finance

* ChatGPT assessment: Financial soundness and market dominance are strong, but innovation lags behind top peers.

📝 Implication: While Apple boasts outstanding financial health and dominance, its relatively slow pace in adopting new technologies raises concerns over its long-term growth and innovation. If Apple falls behind in AI and cloud leadership, it may struggle to maintain its tech premium.

📌 Conclusion Summary

Short-term: Focus on risk management rather than expecting a technical rebound.

Mid-term: Watch for Apple's AI strategy overhaul and year-end events (WWDC, AI chip announcement, etc.).

Long-term: While cash flow and capital efficiency remain strong, the tech premium may weaken among mega-cap peers.

This report is for informational purposes only and does not constitute investment advice.

The analysis is based on data from ChatGPT, TradingView, Investing.com, and Yahoo Finance.

All investment decisions are solely the responsibility of the reader.

로켓랩(RKLB) 2025 매출 $602M·수주잔고 +73% — Neutron Q4 2026 발사 점검 로켓랩(RKLB) 2025 매출 $602M·수주잔고 +73% — Neutron Q4 2026 발사 점검 Neutron 첫 발사가 2026년 4분기 로 연기된 지 약 5개월이 지났습니다. 수주잔고 $1.85B(+73% YoY) 의 폭발적 성장세, 현금 $1.1B 의 든든한 실탄, 그리고 SpaceX 사이에서 찾은 로켓랩만의 생존 공식을 정리해 봅니다. 분석가 중앙값 목표가 $88.88 대비 지금이 매수 메리트가 있는 구간일까요? 📌 모니터링 5개월차 — 서두를 필요가 없는 이유 안녕하세요, 30대 진도리에 취미생활 의 미니도리몽입니다. 필자는 로켓랩(NASDAQ: RKLB )을 2025년 11월 Neutron 발사 연기 발표 이후 약 5개월간 포지션 없이 추적해 왔습니다. 그 사이 주가는 1년 동안 약 +250% 의 가파른 랠리를 보여주었죠 (Motley Fool, 2026-04-19 기준) . 하지만 최근 $80~90 저항권 에서 차익실현 매물이 출회되며 숨 고르기에 들어간 모습입니다. 이번 글에서는 2025 연간 실적 확정치 → SpaceX 공존 포지셔닝 → 5월 14일 Q1 실적 발표 전 점검 포인트 순서로 함께 살펴보겠습니다. 🚀 SpaceX와 경쟁이 아닌 “필수 대체재” 전략 시장은 흔히 Neutron을 Falcon 9의 대항마로 보지만, 실제 비즈니스 관점은 다릅니다. Falcon 9는 2025년 한 해에만 165회 발사했고 (Aerospace America, 2026) , 내부 발사 비용이 약 $15M으로 추정돼 가격 경쟁만으로는 격차가 뒤집...

🔹 오늘의 핵심 3줄 요약 오클로는 사용후핵연료 재활용 기반의 SMR 기술로 에너지 시장에서 독보적인 위치를 구축 중입니다. 최근 AI 반도체 시장 진출과 맞춤형 칩 설계 역량으로 새로운 성장 모멘텀을 확보하고 있습니다. 주가가 최근 $55 이상으로 상승하며 기존 목표가를 초과했으나, 과열 구간일 수 있어 신중한 접근이 요구됩니다. 🔹 AI 활용 안내 본 글은 ChatGPT의 정보 요약 기능을 활용하여 기본 데이터를 정리한 후, 작성자의 개인 해석과 의견을 기반으로 분석 및 편집되었습니다. 본문에 포함된 그래프와 점수는 공개 데이터를 바탕으로 한 주관적 분석 결과로, 투자 권유가 아닌 참고용 시각 자료입니다. AI가 제공한 정보는 참고용이며, 결론과 투자 판단은 작성자의 주관적인 의견이 포함되어 있습니다. AI 데이터센터 전용 원자로? 오클로의 미래는 어디까지? 🔹 필자의 시선 오클로는 원자력 발전이라는 보수적 산업군과 AI 반도체라는 최첨단 시장을 동시에 겨냥하고 있는 매우 독특한 종목입니다. 기술력 자체는 강력하나, 규제 리스크와 시장의 보수적인 수용성은 여전히 과제로 남습니다. 하지만 향후 AI 서버/엣지 디바이스에 소형 원자로와 AI 가속기를 함께 제공하는 형태의 '하이브리드 전력 솔루션 기업'으로 진화할 수 있다면, 단순 발전회사를 넘어 Tech-Growth 주로 재평가받을 수 있는 여지도 충분합니다. 🔹 기업 개요 기업명 Oklo Inc. (티커: OKLO) 산업 차세대 소형모듈원자로(SMR, Small Modular Reactor) 설립 2013년, 미국 캘리포니아주 팔로알토 CEO Jacob DeWitte (MIT 출신 원자력공학자) 기업 미션 친환경적이며 경제적인 소형 원자로를 통해 전력 인프라 혁신 📊 주요 사업 및 기술 Aurora 파...

샌디스크(SNDK) +288% 랠리 D-day — NAND ASP 가이던스 점검 샌디스크(SNDK) +288% 랠리 D-day — NAND ASP +70% 가이던스 vs $1,080 분석가 목표가 점검 오늘( 2026-04-30 ) 장 마감 후 샌디스크가 Q3 FY26 실적을 발표합니다. 옵션시장은 발표 직후 주가에 ±21% 변동성을 반영 중이고, YTD +288% 랠리는 모두 “NAND ASP가 정말 +70% 오르는가” 라는 한 가지 질문으로 수렴하고 있습니다. 가이던스 상단 돌파 시 쇼트 스퀴즈, 컨센서스 미달 시 32% 조정 — 어느 쪽 시나리오에 베팅해야 할까요? 📌 분사 직후부터 본 종목, +288% 랠리에 진입 못한 이유 안녕하세요, 30대 진도리에 취미생활 의 미니도리몽입니다. 필자는 샌디스크(NASDAQ: SNDK )를 2025년 2월 21일 WDC에서 분사한 직후부터 모니터링해 왔습니다 (Sandisk Investor Relations, 2025-02-24) . 하지만 $30 부근에서 시작한 주가가 1년 만에 $1,000을 넘어서는 폭주 를 보이며 매번 “이미 늦었다”는 판단으로 진입을 미뤘습니다. 4월 29일 종가 $1,064.21 , YTD +288% — 그리고 오늘이 변곡점입니다 (MarketBeat·Yahoo Finance, 2026-04-29) . 이번 글은 두 가지 질문에 답하는 형태로 정리했습니다. WDC 분사 후 NAND 전업 기업으로서, 마이크론 대비 프리미엄 받을 만한 기술적 해자·공급망 우위가 있는가? 오늘 가이던스가 쇼트 스퀴즈를 유발할 만큼의 이익 가속화(NAND ASP 상승)를 증명할 수 있는가? 두 질문의 답에 따라 “지금 따라가야 ...

댓글

댓글 쓰기